Review: bunq Business

Find out if bunq satisfies your business banking needs in our in-depth review

Review by

![]()

Head of Fintech Research

Published: 05.02.24

Updated: 26.02.24

Published: 05.02.24

Updated: 26.02.24

bunq Bank: General Information

bunq is a mobile-first digital bank headquartered in Amsterdam, the Netherlands. Founded in 2012 by a tech entrepreneur Ali Niknam, bunq received a full-fledged banking license from the Dutch National Bank in 2015. The company has since grown into a leading European neobank available in more than 18 countries, reaching a grand total of over €1B in assets under management back in March 2021, €2,5B in early 2023 and reaching total customer deposits of over €4,5B in January 2024.

bunq has since updated the plan structure and expanded their portfolio of financial products, becoming the first challenger bank to provide mortgages to customers in the Netherlands. Today, this rapidly growing bank offers a variety of plans for businesses, entrepreneurs, freelancers and self-employed workers.

bunq: Key Facts

| Founded | 2012 |

|---|---|

| Headquarters | Amsterdam, NL |

| Customers | 17'000'000+ |

| Website | bunq.com |

| Personal Banking | Free plan available |

| Business Banking | Free plan available |

| Sign-up Bonus | 30 days free |

| Web Client | ✔️ |

Exclusive offer for Fintech Compass visitors: 30-day free trial

To benefit from the offer, simply follow any of the bunq links on our website .

bunq offers online banking for individuals and businesses, with both desktop (web) version and Android & iOS apps available in Europe. bunq's full official banking license is granted by a regulatory body from the Netherlands (the Dutch National Bank) and is valid all over the EU.

Companies opening a bank account at bunq automatically get an account with a Dutch IBAN (International Bank Account Number), however, businesses based in Germany, France and Spain get IBANs from these countries. bunq's "Local IBANs" allow your business to open bank accounts in multiple countries, which might be advantageous for tax purposes.

For this review, we assembled a broader than usual team of 5 digital finance and banking experts, had them set up bunq business accounts and trial it for two weeks. We then wrote down their feedback, analyzed it, combined these assessments with insights picked up from user reviews found online and condensed all of this in a concise article. Would bunq satisfy your business banking needs? Find out by reading our review below so you can make an informed choice yourself.

bunq: Availability per country

Legal business entities registered in the following countries can sign up for a bunq bank account for businesses:

Austria

Belgium

Bulgaria

France

Germany

Greece

Ireland

Italy

Netherlands

Portugal

Slovakia

Slovenia

Spain

Denmark

Finland

Norway

Sweden

Iceland

Review: bunq for personal banking

Considering a personal bank account at bunq? Explore plans offered for individuals and all the applicable fees and get to know all the features available at bunq in our concise, yet detailed review.

bunq Business: Plans Available

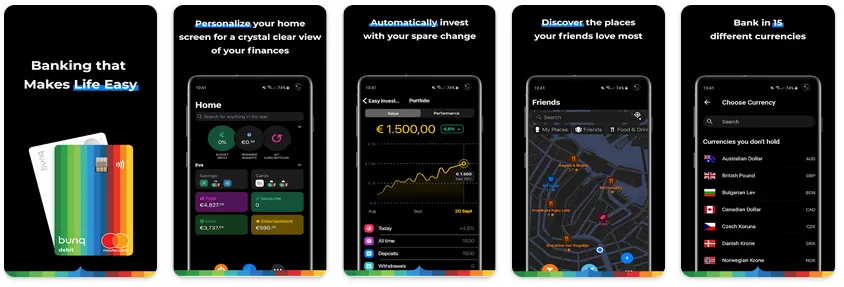

bunq offers a grand total of four options available for both individuals and companies. They have straightforward names that reinforce the concept bunq pushes through: managing company expenses should not take your time away from focusing on the core products and services your business offers, while banking can (and should) be easy.

The four are: Easy Savings (technically, it is a savings account, not a full-fledged checking/current account), Easy Bank, Easy Money and Easy Green. We'll provide an overview of the main differences in bunq subscriptions below.

bunq Easy Savings Business

No monthly cost

Easy Savings is a savings account that allows you to earn up to 1,05% (or 2,46% for NL & up to 3% for DE users) interest on your deposits, paid out to your account every week. And while you can use Apple's Tap to Pay, and your money is fully covered by the Deposit Guarantee Scheme, you don't get a "full" bank account with this plan, meaning you can't execute bank transfers, accept and send payment requests or pay with your bank card. In that sense, bunq Easy Savings is more of an investment tool rather than a proper bank account. To get one, you'd have to upgrade to any of the following three plans.

bunq Easy Bank Business

€ 6.99 per month

bunq's baseline plan, Easy Bank, is an inexpensive option that gives a good impression of what bunq's about while still comfortably covering a freelancer's basic banking needs. Significantly less powerful than the higher-tier plans, Easy Bank is still a solid product that has an impressive array of niche features, while performing very well in day-to-day banking. bunq cards have a high international acceptance rate, you get things like instant notifications, iDeal, blocking/unblocking and even changing your card's PIN on the fly, all secured by industry-standard hi-tech security measures.

Would bunq Easy Bank be enough to satisfy your business banking needs? After reviewing all the differences (seen in a table below), our call is that you can indeed use this modestly-priced subscription without feeling too restricted. That is, provided you run a simple operation that doesn't require multiple sub-accounts for basic cash flow management, your business doesn't pay in currency and you rarely, if ever, withdraw cash from via an ATM. However, there absolutely is immense value in our next plan called ...

Bank Accounts for Businesses

Time is money if you're a business owner, franchisee or a freelancer. Discover modern mobile-first bank accounts for companies of any scale and explore unique features and products built for digital-native business owners.

bunq Easy Money Business

€12.99 per month

Easy Money is a plan that helps you run your business with ease from anywhere in Europe. With easy accounting thanks to bookkeeping software integrations, an ability to auto-sort your VAT to store it in a separate sub-account till the tax season comes and an array of other "make your life easier" benefits, Easy Money is a significant improvement over Easy Bank.

Also included in this in subscription: multiple physical and virtual bank cards with global acceptance, Apple Pay & Google Pay, an array of local payment methods (including iDEAL, SOFORT and Bancontact) and an ability to create up to 25 standalone bank accounts each with its individual IBAN. On top of that, you get up to 25 virtual cards, 1% cashback on HoReCa payments, automated invoice scanner, ZeroFX for great exchange rate when paying in currency, budgeting features and more! The price bites, but it's very easy to justify the cost for a lot of business users.

Our verdict is straightforward: Easy Money is easily the best value for money bunq has to offer. premium-tier business bank account is a great choice for hassle-free business banking.

Easy Green Business

€22.99 per month

Easy Green is bunq's top-of-the-line account at a premium price point. The main advantage over the mid-tier Easy Money plan is an ability to effortlessly offset your CO2 emissions thanks to automatically planting a tree for every €100 spent from your bunq Business account. On top of this, Easy Green features invoice scanning using your phone's camera, extended warranty and purchase protection.

Beyond the CO2 offset and a few other "green" features, the only difference between the two is Easy Green offering 2% cashback on all public transportation transactions.

This subscription feels "light" on additional benefits compared to more reasonably-priced options like Easy Money and Easy Bank, and our opinion is as follows: if you're not looking to up your sustainability game, you are better off with a more affordable alternative, bunq Easy Money, easily the best value-per-euro plan offered by bunq.

Looking to compare the best business banking offers available today? bunq's bank accounts for companies are also featured in our selection of in-depth "one-on-one" comparisons. Find the list of comparisons of bunq bank accounts by going to the links below:

Business banking solutions offered by bunq vary significantly both in features available, business types they target (with Easy Bank being a better fit for freelancers), and, of course, in price. Find a detailed breakdown of all bunq plans offered to businesses in our comparison table below.

bunq: Plan Comparison Table (Business)

| Feature | Core Business | Pro Business | Elite Business |

|---|---|---|---|

| Price, per month | € 7.99 | € 13.99 | € 23.99 |

| Commitment | Cancel monthly | Cancel monthly | Cancel monthly |

| Sign-up bonus | 30 days free | ||

| Website | bunq.com | ||

| Accounts | |||

| IBANs | NL, DE, FR, ES, IE | NL, DE, FR, ES, IE | NL, DE, FR, ES, IE |

| Sub-accounts included | 2 | 25 | 25 |

| Shared Access | No extra cost | Up to 10 people | Up to 10 people |

| Employee Accounts | ✔️ | ✔️ | ✔️ |

| Mobile Payments | |||

| Apple Pay | ✔️ | ✔️ | ✔️ |

| Google Pay | ✔️ | ✔️ | ✔️ |

| Samsung Pay | ❌ | ❌ | ❌ |

| Other methods | - | - | - |

| Cards | |||

| Cards available | Mastercard | Mastercard | Mastercard |

| Cards included | 1 | 3 | 3 |

| Maestro/VPay | ✔️ | ✔️ | ✔️ |

| Debit cards | ✔️ | ✔️ | ✔️ |

| Credit cards | ✔️ | ✔️ | ✔️ |

| Virtual cards | ✔️ | ✔️ | ✔️ |

| Extra card fee | € 3.49 p/m | € 3.49 p/m | € 3.49 p/m |

| Replacement fee | € 9.99 | € 9.99 | € 9.99 |

| Free replacements | - | 1 per year | 1 per year |

| Metal card | ❌ | ✔️ | ✔️ |

| Wooden cards | ❌ | ❌ | ❌ |

| Payment Methods | |||

| iDeal | ✔️ | ✔️ | ✔️ |

| SOFORT | ✔️ | ✔️ | ✔️ |

| Bancontact | ✔️ | ✔️ | ✔️ |

| Various Fees | |||

| SWIFT (receive) | € 5.00 | € 5.00 | € 5.00 |

| Foreign exchange fee | 0.50% | 0.50% | 0.50% |

| Currency fee-free limit | - | - | - |

| ATM Withdrawals | |||

| Daily limit | € 1,000 | € 1,000 | € 1,000 |

| Free withdrawals, per month | - | 6 times | 6 times |

| After that, per withdrawal | € 0.99 | € 0.99 | € 0.99 |

| Withdrawal fee abroad | € 2.99 | € 1.99 | € 1.99 |

| Interest Rate | |||

| Current accounts | ❌ | ❌ | ❌ |

| Savings accounts | 1.05% | 1.56% | 1.56% |

| Transaction & Deposit Limits | |||

| Deposit limit | - | - | - |

| Deposit Protection | Up to €100'000 | ||

| Monthly spend limit | - | - | - |

| Other financial products | |||

| Overdraft | ❌ | ❌ | ❌ |

| Investments in-app | ❌ | ✔️ | ✔️ |

| Crypto trading | ❌ | ❌ | ❌ |

| Cheques | ❌ | ❌ | ❌ |

| Cashback | ❌ | 1% on HoReCa | 1% HoReCa, 2% transport |

| Insurance | ❌ | ❌ | Travel |

| Lounge access | ❌ | ❌ | ❌ |

| Transaction categorization | ❌ | ✔️ | ✔️ |

| Purchase protection | ❌ | ❌ | Extended Warranty |

| Round-up savings | ❌ | ✔️ | ✔️ |

| Cash Flow Control | ❌ | ✔️ | ✔️ |

| Deals & Discounts | ❌ | ✔️ | ✔️ |

| Other benefits | Director access, Wise | Add-ons, Auto-VAT | Auto-CO2 offset |

| Learn more |

Go to bunq.com

| ||

Unique Benefits: bunq for Businesses

Tap to Pay (available on iPhone)

Using Tap to Pay, you can easily accept contactless payments with just your iPhone and a bunq app. "Physical" debit and credit cards, Apple Pay and Google Pay can all be collected using your iPhone. This feature requires no additional set-up and works wonders for these who need an option to start accepting cards as soon as possible, but do not expect the volumes that justify getting a standalone card reader.

Available on every bunq plan (including the free Easy Savings subscription!).

Invoice Scanning

Received an invoice you need to pay? You can open the bunq app, tap on the "Camera" button and select "Pay Invoice". The OCR algorithms will then scan the invoice and pre-fill your bank transfer details (including the counter-party name, bank account details and the amounts). This feature alone can save you a significant amount of time if you find yourself frequently paying invoices and inputting the details manually.

Available on Easy Money & Easy Green.

Auto-VAT and Auto-Export

Two similar features - "Auto VAT" makes managing your VAT a breeze by automatically setting aside the VAT amount (variable and adjustable) on both incoming and outgoing payments into a dedicated account That way, the moment you need to submit your VAT declaration, you already have the funds prepared.

Auto Export is a feature that lets you set up an email address you want your bank statements to be forwarded to, and bunq will then automatically send these as soon as they become available. Very useful in case your business uses an external bookkeeper and makes accounting a breeze for you.

Bookkeeping Integrations & Zapier

Not a coder, yet want to enjoy the "smart and automated" banking experience? This is now easily achievable, thanks to bunq's integration with Zapier. Adding a row to a Google Sheets table whenever a transaction is executed? Easily set up in less than 10 minutes! Sending a Slack message when receiving a payment? Say no more! On top of that, bunq supports quite a few pieces of bookkeeping software with more being added every couple of months.

bunq bank cards we used - metal credit card and a plastic Maestro.

bunq: Pros & Cons

Advantages

Cash flow control: In case you opt for either Easy Money or Easy Green plans, it is very easy to set up a few sub-accounts for splitting up your expenses into very straightforward standalone bank accounts. Thanks to automatic transaction categorisation, an ability to split up funds related to different trade names while still having them all in one account within a single app and features like Payment Splitter, you will never wonder where you spent that much money last month.

Cash flow control: In case you opt for either Easy Money or Easy Green plans, it is very easy to set up a few sub-accounts for splitting up your expenses into very straightforward standalone bank accounts. Thanks to automatic transaction categorisation, an ability to split up funds related to different trade names while still having them all in one account within a single app and features like Payment Splitter, you will never wonder where you spent that much money last month.- Tap to Pay, bunq.me links and recurring payment requests combine to make for easy payment collection.

- Local IBAN and bank details: bunq users from Germany, The Netherlands, Spain and France get to enjoy having local IBANs (for example, starting with "NL97 ..." for The Netherlands) for their sub-accounts with bunq, which is not the case for most neobanks on the market (N26 users get DE IBAN no matter where they are, same as Revolut's Lithuanian bank accounts).

- Freedom of Choice: bunq advocates for ethical investment practices and aims to empower its users to follow suit. You can choose where you want your deposits to be invested (you are also free to disable getting interest) right in the bunq app at any time.

- 3 physical and up to 25 virtual cards already included in your Easy Money & Easy Green subscription.

Downsides

No invoice generation - you will need to continue making these manually or connect an accounting software of your choice.

No invoice generation - you will need to continue making these manually or connect an accounting software of your choice.- Too many things: bunq offers an exceptional collection of features, but the downside of this approach (given bunq's fairly limited employee headcount) is that certain features introduced over a year ago sometimes get zero maintenance and their quality and reliability eventually decreases up until bunq decides to revamp and update that functionality.

- Unintuitive app UI: in an effort to make things as easy as possible without overwhelming the user, bunq's product team sometimes makes quite mind-boggling calls, resulting in some functionality being hidden so deep down in the app, you might not even know it is actually there. You do get used to the core features quite fast though, and you might even find the way they are arranged convenient after some time, but there is a steep learning curve before that.

- Not cash-friendly: very limited options to deposit cash into your account, and very conservative ATM withdrawal limits.

Multiply Your Wealth

Doesn't matter if you're just saving up for that summer vacation or if you're planning your retirement, the best time to start investing is now. Explore our curated list of the best investment platforms and apps available today at Fintech Compass. Make your money work so you don't have to.

bunq Business: Frequently Asked Questions

Does bunq offer real bank accounts for businesses?

bunq B.V. holds a full banking license provided by one of Europe's most reliable and respected banking authorities, the Dutch National Bank. This means that all customer's deposits (capped at €100'000 per account) are fully insured via DNB's Deposit Guarantee Scheme and backed by the government of the Netherlands. On top of this, this license ensures that the challenger bank is subject to a high level of scrutiny and intense audits by regulators. So yes, bunq is a real bank that offers fully-licensed and regulated bank accounts for both companies and individuals.

Will I get a Dutch IBAN when signing up for bunq?

Despite being a Dutch bank, businesses registered in Germany, France and Spain get local IBANs, which is a unique benefit as far as mobile-first banks go. Users from other countries get a Dutch IBAN (which begins with "NL97 ..."). You can also get bank accounts in multiple countries at bunq, but that (admittedly, quite niche) option incurs an additional cost. And in case you were wondering, IBAN is an abbreviation that stands for "International Bank Account Number".

Are there hidden fees and unforeseen charges at bunq?

Most of your "day-to-day" features available at bunq are included in your subscription cost. That means, you can send and receive money via SEPA bank transfers, send payment requests, use Apple Pay or Google Pay, execute payments via iDeal, SOFORT and using your bank card online without any limits. The only charges to be aware of are (assuming normal usage) for accepting credit card payments using your bunq.me link (2,5% fee), withdrawing money from an ATM more than 6 times a month, receiving SWIFT payments (a flat €5 fee) and ordering more than 3 physical cards.

Does bunq offer a credit card?

The answer is ... "yes and no". While bunq does offer a Mastercard Credit card, you can not open a credit line or enable overdraft. Why would it be an option then? It still has niche use cases as certain vendors (most commonly, car rental companies, hotels and any other business that "freezes" an amount on your card prior to the actual payment) often require you to pay specifically with a credit card. As an added bonus, credit cards from Mastercard have the best worldwide acceptance.

How do I contact bunq support?

bunq support can be contacted 24/7 via the in-app chat in any of the six languages bunq supports. As an alternative, it is possible to email bunq with any questions you might have at support@bunq.com. bunq's address is 1043 BS Amsterdam, Naritaweg 131-133, The Netherlands. You can report bunq scam and fraud by bunq users on bunq's website.

Which countries is bunq business available in?

Individuals residing in the following countries with a registered business can use bunq: the Netherlands, Belgium, France, Germany, Austria, Spain, Italy, Portugal or Ireland. The list is constantly expanding, so make sure to check bunq's official website or app listing for up-to-date information.

bunq Business: Top Alternatives

Does the feature set of bunq lack something you are explicitly looking for? Perhaps, you are looking for a company account in a different price range? Or do you want to find a more powerful solution for your needs? Below, we will provide you with three bunq alternatives other business owners found the most fitting.

Finom

Finom is a Dutch neobank for SMEs and freelancers, offering an elegant solution to expense management woes to businesses of any scale. You can connect all of your bank accounts thanks to Open Banking integrations to have a complete overview of your cash flows, and enjoy automated invoice generation, saving valuable hours you'd otherwise spend on payment collection. Next to it, convenient UI on both desktop and via mobile apps, multi-user access and your new bank account with its own IBAN. Free plan is also available, which makes it easier to try Finom without any risks.

Finom

Finom offers digital banking with built-in invoicing and expense management solutions for freelancers, self-employed and entrepreneurs, SMEs and companies under registration.

![]()

![]()

General Information

- Deposit ProtectionUp to €100'000

- Customer SupportChat, Whatsapp, Email

- CurrenciesEUR

Bank Accounts

- Individuals

- Businesses Free plan available

- Joint

- Convenience & User-friendliness

- Customer Support

- Features Available

- Value for Money

- Overall Rating

Qonto

Qonto is a French digital bank for entrepreneurs, freelancers and SMEs. This neobank's on a mission to simplify and digitize the stagnant banking system. Remarkable selection of plans, ranging from affordable options for self-employed professionals all the way to customizable Enterprise-level solutions. Invoice creation and payment automation, expense management solutions and tools to facilitate easy bookkeeping - Qonto truly has it all.

Qonto

Qonto is a French neobank for businesses that is equally suited for freelancers, micro-businesses, SMEs and startups. Diverse in its product portfolio and capable of satisfying business needs of any caliber, Qonto now offers a one-month free trial for new users.

![]()

![]()

General Information

- Deposit ProtectionUp to €100'000

- Customer SupportPhone, chat, email

- CurrenciesEUR

Bank Accounts

- Individuals

- Businesses Starting at €9.0

- Joint

- Convenience & User-friendliness

- Customer Support

- Features Available

- Value for Money

- Overall Rating

Revolut

Unsurprisingly, we just can't ignore Europe's largest neobank, Revolut. A true staple of mobile-first banking, Revolut boasts having an army of 500'000 businesses it powers. With a free plan, an ability to create your account in mere minutes and dozens of countries supported, Revolut is always a solid choice when it comes to managing your company's finances.

Revolut

Europe's biggest neobank, Revolut is a pioneer of mobile-first banking. Offering a wide range of financial services and banking products, including (but not limited to!) trading stocks and crypto, Revolut is a safe option regardless of customer's country of residence.

![]()

![]()

General Information

- Deposit ProtectionUp to £85'000

- Customer SupportChat, email

- Currencies30+ currencies

Bank Accounts

- Individuals Free plan available

- Businesses Free plan available

- Joint

- Convenience & User-friendliness

- Customer Support

- Features Available

- Value for Money

- Overall Rating

Verdict: Is bunq right for your company?

bunq surely does not lack the features nor does it struggle to justify the price tag (which is more or less similar to what's offered by bunq's competitors). An abundance of "smart banking" features, all the "bread and butter" day-to-day functionality you would expect from your bank in a digital age and a commitment to ethical investment practices along with a focus on sustainability - what more could a business need?

On the other hand, bunq's downsides (namely, overall cash-"unfriendliness" and a very basic desktop app) might be off-putting enough to become deal-breakers for some business owners, especially combined with the less significant drawbacks (e.g. confusing app UI or lack of Garmin Pay or Fitbit Pay). The company is also constantly innovating, and you can feel that nothing is truly "set in stone" at bunq in terms of UX/UI with the neobank always trying to improve the end users' experience, which can be a bit overwhelming at times.

However, greenwashing (bunq does like mentioning tree planting and going CO2-neutral... a lot) and the "social banking" experiments aside, bunq remains a solid high-tech neobank with a full-fledged banking license provided by a trustworthy regulatory authority in one of the safest countries, thanks to established judicial system and the strength of its economy. Frequently dismissed by businesses due to its flashy and "funky" visual style, in its core, bunq is an extremely robust and powerful bank that gets better the more you "settle in" and acquaint yourself with a wide range of possibilities to choose from.

At the end of the day, choosing a bank account for your business is an important decision that will have a major impact on your company's financials. Which is why it is worth your time to get "hands-on" with multiple alternatives and stick with the one that suits you best, based on your own assessment. And with that approach, we can definitely vouch for bunq being a solid addition to your consideration set.